As 2025 ends, I want to pause, not just to reflect on the year behind us, but to share how intentionally we are building what comes next.

At Three Creeks, progress is never accidental. Every improvement we make, every service we add, and every decision behind the scenes is made with one goal in mind: helping you feel confident, organized, and prepared for the future.

This year, our focus shifted from simply growing to growing better.

Here’s what that looked like in practice:

Deeper Tax Planning: We significantly expanded our tax planning work—helping clients identify multi-year strategies, coordinate charitable giving, and make smarter decisions around income, distributions, and timing.

Estate & Legacy Strategy Enhancements: Many clients updated estate planning strategies using tools like Donor Advised Funds and Qualified Charitable Distributions, aligning wealth with values while improving tax efficiency.

Client Experience Investments: We added new roles and technology focused entirely on improving communication, follow-through, and the overall client experience—so every interaction with Three Creeks feels clear, proactive, and personal.

Charles Wan, CFP® (Registered Professional) came on board in July and is already having a big impact on the business and for clients.

Raising the Bar Internally: Todd was part of Strategic Coach throughout 2025, working alongside top entrepreneurs and advisors nationwide to sharpen the vision, systems, and long-term strategy for Three Creeks Capital. This investment is already shaping how we think, plan, and serve. For 2026, Todd has joined The Perfect RIA Freedom program to continually improve the client experience, internal systems and process, so that clients and employees have great experience.

Looking Ahead to 2026

As we enter the new year, our focus is clear:

Even more proactive tax planning, webinars and client communications. We have added texting software so that clients can text all business-related information to the office phone number.

Continued estate and legacy strategy updates, especially with the recent tax law changes.

Further investments in technology and people to enhance service and responsiveness

Expanded education and communications you always understand why we’re recommending what we do. We will host four webinars in 2026 (Roth Conversions, Travel Insights for the Travel Enthusiast, Market Updates and Tax Planning to Avoid Overpaying the IRS.)

Enhancing our YouTube Channel for client education purposes and looking forward to meeting with the client advisory board in Q1 to discuss further enhancements.

Most importantly, we remain committed to thoughtful, long-term planning, not reacting to headlines but helping you make decisions that support the life you want to live.

Thank You for Your Trust

We don’t take lightly the responsibility of advising you and your family. Your trust is the foundation of everything we do, and we are grateful to walk alongside you as your lives and financial strategies evolve.

In the coming weeks, we’ll be reaching out to schedule reviews, tax planning conversations, and planning updates as we head into 2026.

Thank you for being part of the Three Creeks family.

Volunteer Spotlight: John Lorenz

John Lorenz is a dedicated Metro Parks volunteer with 35 years of service, who was named All-Metro Parks Volunteer of the Year in 2020.

Background: He grew up in Grandview Heights, studied Environmental Interpretation and Natural Resources at OSU, and had a long career in electronics and computer networking (repairing organs, then Commodore 64s, and finally network management for companies like Hirschvogel).

Volunteer Work: His involvement started in 1989 at Battelle Darby Creek Metro Park after attending a seining program. He has volunteered in various capacities, including:

Leading canoe floats and seining programs.

Assisted Stream Quality Monitoring (SQM) workshops by helping to train citizen volunteers to identify the various benthic macroinvertebrates.

Inventing and making acrylic viewing boxes and SQM ID sorting trays for naturalists.

Participating in vernal pool surveys and invasive plant removal (his main activity now).

Memorable Moments: He cherishes his early family canoe floats and mussel noodling, and recounts amusing stories like a longnose gar swimming up a child's shorts during a seining program.

Personal Life: He lives in Upper Arlington with his wife, Karen (who also volunteers). They have three children and five grandchildren. They enjoy traveling (especially to Maui and on Viking River Cruises) and hiking. He is an avid cook, baker, and gardener, even raising mason bees and having a pet tiger salamander named Gollum for 10 years.

WEP/GPO Repeal: What It Means for Our Ohio Public Employees Community

There peal of the Windfall Elimination Provision (WEP) and the Government Pension Offset (GPO) that have affected public employees for decades is one of the most significant Social Security changes in recent history. For many of our Ohio public pension members this repeal represents long overdue financial relief.

Quick Recap: What Were WEP and GPO?

Windfall Elimination Provision (WEP) WEP reduced Social Security benefits for individuals who worked in jobs not covered by Social Security (Ohio pension system) but who also had enough Social Security credits from other employment.

The intent was to prevent “double dipping.”

In reality, it often penalized first responders who had legitimately earned Social Security credits through second careers, military service, or part-time work.

The reduction could be as high as $557/month in 2025 (depending on years of substantial earnings).

Government Pension Offset (GPO) GPO reduced or even eliminated Social Security spousal or survivor benefits for individuals receiving a government pension.

It offsets Social Security benefits by two-thirds of the pension amount.

Many surviving spouses received little or no Social Security income because of this rule, even when they had paid into the system for years.

What the Repeal Means Going Forward

With the repeal now in effect:

Social Security benefits for affected workers will be calculated using the standard formula, not the reduced WEP version.

Spousal and survivor benefits will no longer be offset by two-thirds of a pension under GPO rules.

Many public employees will see meaningful increases in Social Security benefits over their retirement lifetimes.

Surviving spouses, especially those depending on survivor benefits, may see the most dramatic improvement.

How This Impacts Our Clients Personally

For our Three Creeks Capital clients who were affected by these rules, the repeal removes a large source of uncertainty and frustration around retirement income planning.

Some will see their Social Security benefits restored fully.

Others will see increases in spousal or survivor benefits that meaningfully change their long-term financial outlook.

For individuals who have spent their careers in the public pension system but worked part-time jobs or military service under Social Security, this may represent a significant additional income source.

Estimated Dollar Impact for Our Client Base

We’re currently analyzing the individual impact across our client households. Based on early projections, the repeal is expected to restore a substantial amount of benefits over our clients’ collective retirement lifetimes.

What You Should Do Next

If you’re unsure how this repeal changes your own retirement plan, especially if you’re in or near retirement, we want to review this with you in 2026 if we haven’t already. Areas we’ll cover during our WEP/GPO update meetings:

Updated Social Security projections

Changes to spousal or survivor income

Revised retirement cash-flow and pension integration

Long-term tax implications

Opportunities for strategy adjustments in 2025 and beyond

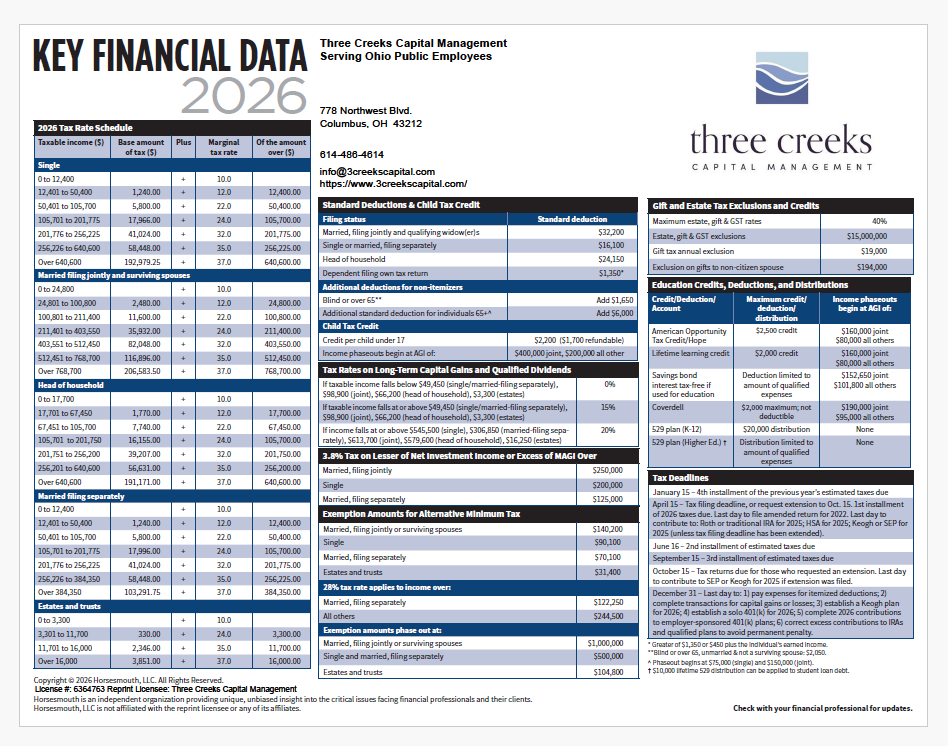

It's All About Tax in 2026

The One Big Beautiful Bill Act (OBBBA), passed on July 4th, 2025,significantly impacts federal taxes, credits, and deductions. Most notably, it makes the Tax Cuts and Jobs Act (TCJA) originally passed by the Trump Administration in 2017 permanent.

So, what does that mean going forward and how can it affect your financial situation?

Eligible seniors 65 and older will now receive up to $6,000 in tax deductions per person. This enhanced deduction may affect strategies revolving around Roth Conversions and Medicare Part B & D premiums.

For individuals and families who are currently still in the workforce, the new State and Local Tax (SALT) deduction cap has been raised from $10,000 to $40,000. As a result, you may benefit from itemizing deductions rather than taking the standard deduction, which could help reduce your overall tax liability.

Given these changes, your overall tax strategy may need to be reassessed. Proactive tax planning is more important than ever, and we look forward to continuing to serve you and your family as we navigate these updates.

Texting Your Advisor (Requirements)

Starting in 2026, we will no longer be able to accept any business-related text messages to our personal cell phones. SEC and FINRA require all forms of communication with a client to be captured.

Specifically, Rule 17a-4(b)(4) requires retention of originals of all communications received and copies of all communications that relate to an advisor’s business — whether email, text, instant message, or chat application. If we do not adhere to these rules, we can be fined and/or suspended.

Anything related to business, not personal, must be sent to the office phone line. All business-related text and calls must go to 614-486-4614. You will not receive a text response if you send a business-related text message to any personal cell phone number(s).

The charitable entities and/or fundraising opportunities described herein are not endorsed by, or affiliated with Cetera Advisors LLC or its affiliates. Our philanthropic interests are personal to us and are not reviewed, sponsored, or approved by Cetera Advisors LLC.

Cetera Advisors LLC exclusively provides investment products and services through its representatives. Although Cetera does not provide tax or legal advice, or supervise tax, accounting or legal services, Cetera representatives may offer these services through their independent outside business. This information is not intended as tax or legal advice.

Click to Talk with an Advisor

Click to Talk with an Advisor