For years, many Ohio public employees believed they would lose Social Security benefits because they earned an OPERS pension. That changed in 2025!

With the repeal of the Government Pension Offset (GPO), many Ohio Public Employees (OPE) retirees may now qualify for Social Security benefits they previously could not receive — including spousal and survivor benefits.

Yes.

Following the repeal of WEP and GPO, many OPE retirees may now qualify for Social Security spousal benefits.

Importantly, a Social Security spousal benefit is not only available after the death of a spouse.

Many Ohio public employees are surprised to learn they may qualify for a Social Security spousal benefit while both spouses are still living.

This is one of the most misunderstood retirement planning topics affecting Ohio public employees today.

A spousal benefit allows one spouse to receive one-half of their spouses Social Security income based on the spouse’s earnings record.

In the past, the Government Pension Offset (GPO) often reduced or eliminated these benefits for OPERS retirees receiving a public pension.

After the 2025repeal, many retirees may now receive:

This change has created new retirement planning opportunities for many Ohio public employees, teachers, administrators, and government workers.

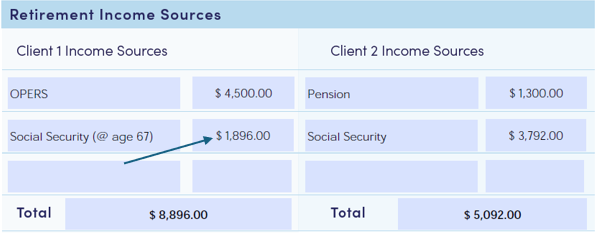

The example below shows how pension income and Social Security benefits may work together for are tired couple after the repeal of the GPO.

Client 1 receives:

Client 2 receives:

Together, these retirement income sources create the household income plan.

Example: OPERS, STRS and OP&F Pension and Social Security Income While Both Spouses Are Living

This is one of the most important retirement income planning questions for married couples.

Many retirees incorrectly assume the surviving spouse continues receiving both Social Security checks.

That is not how Social Security survivor benefits work.

Instead:

Understanding this rule is critically important when planning long-term retirement income for married couples.

A Social Security survivor benefit allows a surviving spouse to step into the larger Social Security benefit after the death of their spouse.

For many public employees, the repeal of GPO may now allow access to survivor benefits that were previously reduced or unavailable.

This creates an important planning opportunity for households where one spouse earned a significantly larger Social Security benefit.

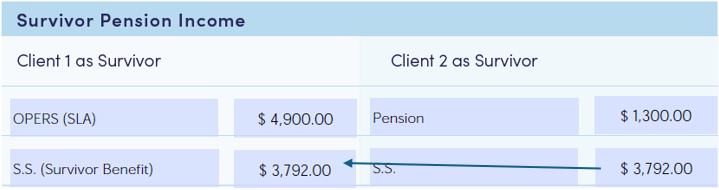

In the example below, Client 1 survives Client 2.

Client 1:

As a result, Client1’s Social Security income increases from the smaller benefit amount to the larger survivor benefit amount.

This is one of the most important retirement income planning concepts for married couples.

In this example, Client 1’s smaller Social Security benefit is replaced by Client 2’s larger survivor benefit after Client 2 passes away.

Why Survivor Income Planning Is Still Critical

Even after the repeal of WEP and GPO, couples still need to plan carefully for:

For many retired households, the largest financial transition occurs after the first spouse passes away.

Understanding how OPE pensions, Social Security benefits, spousal benefits, and survivor benefits work together is essential to building a successful retirement income strategy.

Click to Talk with an Advisor

Click to Talk with an Advisor